Strategic Resilience in an Age of Geopolitical Disorder

Executive Summary

Strategic resilience has become a core leadership capability, yet many resilience discussions remain too narrow. The external environment is no longer defined by isolated shocks that can be absorbed and then left behind. It is defined by overlapping disruptions: geopolitical confrontation, geoeconomic coercion, political volatility, technological concentration, climate extremes, social divides and the weakening of rule-based coordination. In such an environment, resilience can no longer mean merely returning to normal. The task is to remain capable of acting, investing, prioritizing and adapting while the environment shifts.

This new environment can be understood through three lenses. The first is predatory power: states and other powerful actors increasingly use disruption, dependencies and asymmetries as instruments of influence. The second is the hidden fragility of large systems: highly optimized economic, technological and political systems often look strong until stress reveals how brittle they have become. The third is the underestimation of obvious but suppressed risks: many of the most consequential risks are not unforeseeable shocks, but have been acknowledged rhetorically and postponed practically for too long.

For companies and organizations, this changes the meaning of strategy. Competitive strength now depends not only on cost, innovation and operational excellence, but also on the ability to recognize coercible dependencies, absorb systemic shocks and adapt before external stress hardens into strategic disadvantage. Strategic resilience has therefore become a core leadership capability at the intersection of strategy, risk, operations, technology, sustainability and governance.

When thinking about and operationalizing resilience five core elements are critical: strategic risk awareness, dependency intelligence, deliberate creation of strategic options, decision velocity and renewal capacity. In parallel, organizations can move forward by a set of principles for action, including selective openness, intelligent redundancy, dynamic adaptation and the integration of climate, AI and foresight into risk management and core decision-making.

A foresight-based approach helps translate this complexity into practical action and demonstrates how short-term strategic orientation can be strengthened without weakening long-term position. It does so by identifying relevant emerging risks early, mapping how they could interact, assessing where impacts are greatest across the organization, and defining concrete options across the full risk timeline: before disruption, during impact and after it. The objective is not to predict one future with false precision. It is to expand room for maneuver across several plausible futures and to improve short-term strategic choices today.

1. The End of Strategic Comfort

The operating environment has changed structurally. Geopolitical and geoeconomic confrontation has moved to the center of short-term global risk perceptions. The present moment should not be misread as a temporary accumulation of crises. The world is moving away from an environment in which markets, institutions and rules did much of the stabilizing work, and toward one in which leverage, coercion and asymmetry increasingly define outcomes. More centers of power do not automatically produce a more balanced world. They can also produce a more transactional, more fragmented and more predatory one. For instance, in a fragmented world, middle powers might act more opportunistically by switching alliances to counterbalance the growing rivalry between the great powers, which limits their room for maneuver.

The first lens for understanding this shift is predatory power. Russia’s war against Ukraine is not only a brutal military conflict; it is an imperial project aimed at demonstrating that violence, terror, attrition and political exhaustion can overturn sovereignty and reopen spheres of influence. The second Trump administration points in a different direction, but toward the same structural conclusion. It has further normalized the use of tariffs, sanctions and executive discretion as instruments of bargaining and economic pressure. China, by contrast, often acts with greater patience and less spectacle. Yet here too the logic is unmistakable: influence is expanded through industrial depth, infrastructural reach, technological scale, standards, finance and the gradual creation of dependencies. These are different styles of power, but they all indicate the same change. Power is no longer exercised primarily through the stabilization of an open order. It is increasingly exercised through the selective use of disruption, pressure and controlled interdependence.

This matters because interdependence itself has changed meaning. For a long time, economic integration was widely treated as a force of moderation. Today it can just as easily become a channel of coercion. Trade routes, critical minerals, energy flows, export controls, cloud infrastructures, payment systems, semiconductor chokepoints and regulatory access have all become potential instruments of statecraft. The world has not become less connected. It has become more politically charged in the way those connections are governed and exploited.

The second lens is the hidden fragility of large systems. Over recent decades, companies, states and societies have built systems designed for efficiency, scale and speed. That model created enormous gains. But it also concentrated risk. The more optimized and tightly coupled a system becomes, the less spare capacity it has to absorb disruption. Supply chains, logistics networks, energy systems, digital stacks and financial architectures often appear robust precisely because their points of failure remain invisible in normal times. Under stress, however, small disruptions can cascade quickly through the whole system. The same is increasingly true of political systems. Polarized societies, weakened trust, disinformation-saturated media environments and fragmented democratic coalitions make decision-making slower, more erratic and more vulnerable to shock. Right-wing populism is part of this wider pattern. It is not only a political trend; it is a driver of volatility that narrows consensus and increases the probability of abrupt reversals in policy areas that matter directly for business and investment.

The third lens is the underestimation of obvious but suppressed risks. Many of the most consequential dangers facing organizations and societies are not black swans. They are visible, advancing pressures that have been intellectually acknowledged and practically deferred. Climate change is the clearest example. It is no longer a slow-moving environmental background issue. It is becoming a direct source of stress for infrastructure, insurance, agriculture, water systems, energy security, health costs, public budgets and territorial stability. Climate change is therefore not merely another geopolitical factor; it is becoming a force that actively reshapes geopolitics by altering the conditions of power, security, dependency and stability. Artificial intelligence belongs in the same category. AI is often discussed as a story of productivity and innovation, but it is equally a story of concentration, dependence and power. Access to chips, compute, cloud, data and talent is becoming strategically decisive, while AI also expands the attack surface through cyber risk, manipulation, disinformation and opaque dependencies. Demographic ageing, infrastructure decay, fiscal strain and social polarization belong to the same family of visible but insufficiently internalized risks. The danger, in other words, lies less in surprise than in delayed action.

Taken together, these three lenses describe a world of permanent disorder and strategic simultaneity. Military confrontation, geo-economic pressure, technological rivalry, climate stress and domestic political volatility no longer arrive one after another. They accumulate, interact and reinforce one another. That is why strategic comfort is over. The question is no longer when the old normal will return. The question is how organizations can remain capable of acting when instability itself becomes normal.

2. Why This Matters for Organizations

For organizations, the new environment changes the geometry of risk. It enters directly into strategy, operations, finance and legitimacy. Exposure no longer sits neatly inside isolated categories such as compliance, supply chain, cyber or sustainability. A tariff can become a margin problem, a sourcing problem, a customer pricing problem and a political problem at the same time. A climate shock can trigger insurance challenges, infrastructure outages, workforce disruption, supplier delays and public scrutiny in one sequence. An AI decision can create productivity gains while simultaneously increasing concentration risk, model dependency, reputational exposure and cyber vulnerability. The boundary between the market environment and the power environment has become far more porous. What once appeared as a purely commercial decision may now carry geopolitical, geo-economic or societal exposure.

Predatory power enters the organization through multiple channels. A tariff is not just a trade issue; it can become a margin issue, a sourcing issue, a pricing issue and a political issue at the same time. Export controls can reshape product roadmaps. Sanctions can alter customer portfolios and financing assumptions. Security-driven regulation can affect investment decisions, technology choices and cross-border partnerships. Even where no formal restrictions exist, companies can find themselves operating in a world in which access, cost and legitimacy are increasingly shaped by statecraft rather than market logic alone.

At the same time, the hidden fragility of large systems is now a business problem. Many organizations have been built for a world of relative stability: lean inventories, concentrated supplier structures, globally distributed production, just-in-time delivery, standardized technology stacks and highly optimized capital allocation. These configurations remain efficient under normal conditions. But under geopolitical stress, climate shocks or sudden regulatory shifts, they can become sources of strategic weakness. A single cloud dependence can turn into a resilience problem. A regional production concentration can become a political risk. A narrow supplier base can become a strategic chokepoint. What was once celebrated as efficiency may in a more coercive world reveal itself as overexposure.

The same is true for the third lens. Many of the risks that now matter most to organizations have been visible for years, but were often treated as secondary, too long-term or too diffuse to shape core strategy. Climate and biodiversity risks were delegated to sustainability teams instead of being embedded in asset strategy, procurement and insurance logic. AI governance was discussed as a matter of ethics or innovation rather than as a question of strategic dependence, cyber exposure and market power. Political polarization was treated as an issue for governments rather than as a force that could directly affect consumer markets, workforce cohesion, regulation and reputation. In a more unstable world, that compartmentalization no longer works.

This changes the strategic question. It is no longer enough to ask how the organization can protect itself against disruption. The more relevant question is how it can preserve and expand its room for maneuver under conditions of geopolitical disorder. That includes the ability to continue investing, adapting, prioritizing and partnering even when the external environment becomes more coercive, more brittle and more politically charged. Strategic resilience begins exactly there.

For European organizations, the challenge is especially acute. They are exposed to Russian aggression, American volatility, Chinese industrial scale, domestic political fragmentation, climate stress and technological dependence at the same time. But the underlying lesson is broader: any organization operating internationally now has to assume that openness alone is not a strategy. Exposure must be managed deliberately.

3. Strategic Resilience Must Be Redefined

In this context, strategic resilience means more than robustness, recovery or continuity. It means the ability to remain capable of choosing and acting under conditions of high uncertainty, fast-moving disruption and political-economic pressure. It is the capacity to absorb shocks without paralysis, adapt faster than the environment changes, and reposition in ways that strengthen future competitiveness.

This definition matters because many resilience discussions remain too narrow. Operational resilience protects continuity. Financial resilience protects liquidity and balance sheet flexibility. Supply-chain resilience protects the flow of goods and inputs. All of that remains necessary. But strategic resilience sits one level above. It asks whether the organization can still invest, innovate, prioritize and change direction when the world becomes less predictable and more coercive.

Five elements are decisive:

1. The first is strategic awareness: the ability to identify and order emerging risks, structural shifts and possible tipping points early enough to matter. Companies are demonstrating that this capability is not abstract. Shell is a well-known historic example. By acknowledging a possible oil crisis scenario and rejecting the idea that oil supply was infinite, Shell was better prepared for the 1973 oil crisis than others. Swiss Re also lives up to this element through its SONAR tool, an internal crowdsourcing platform that systematically gathers input across the organization to identify emerging risks at an early stage. Swiss Re’s ten-year SONAR review shows for instance that pandemic risks had been flagged long before the outbreak of the COVID-19 pandemic.

2. The second is dependency intelligence: a clear view of the competences, technologies, partners, customers, infrastructures, geographies and input factors like materials on which the organization depends. Toyota’s experience demonstrates how shocks can be converted into dependency intelligence capabilities. Following the 2011 Tohoku earthquake and tsunami, the company faced severe supply chain disruptions, most critically the shutdown of a key semiconductor supplier. Afterwards, the company systematically analyzed its supply chain to identify critical vulnerabilities, resulting in a list of around 1,500 components that required either alternative sourcing or strategic stockpiling. A move that allowed Toyota to cope with chip shortages better during the COVID-19 pandemic and to cope with risks like export restrictions, e.g. regarding Nexperia Chips in China.

3. The third is optionality: the deliberate creation of alternatives in footprint, sourcing, partnerships, capabilities and market exposure. A prominent example is Apple’s gradual shift in its manufacturing strategy. For decades, the company relied heavily on China as its primary production base, benefiting from scale, efficiency and a dense supplier ecosystem. In recent years, however, Apple has expanded production in countries such as India and Vietnam and diversified parts of its supplier network in response to geopolitical tensions and supply chain risks. In essence, Apple is not exiting China, but complementing it—creating geographical optionality so that production can adapt under changing political and economic conditions.

4. The fourth is decision velocity: forward-looking governance that allows organizations to decide and act across silos when conditions shift rapidly. Haier redesigned its organization after recognizing that hierarchical structures slowed decision-making in fast-changing markets. Its RenDanHeYi model follows two principles: first, connecting employees directly to customers and second, everyone has an entrepreneur mindset. The former hierarchical pyramid was replaced by over 4,000 highly autonomous micro-enterprises of 10 to 15 people. Each micro-enterprise defines its own strategy, including which opportunities to pursue and which partnerships to establish. Independent micro-enterprises provide services (e.g., legal support) to those developing customer-facing solutions. This decentralized model helped to overcome the risk of bureaucracy and enables fast decision-making close to the customer.

5. The fifth is renewal capacity: the ability to learn from disruption and convert stress into stronger positioning, rather than merely returning to a previous state. While this capability is often illustrated at the firm level, the renewable energy sector provides a compelling system-level example. Referring to the concept of antifragility, UBS describes how parts of the renewable infrastructure industry in the United States has not only withstood repeated headwinds like policy changes or even U-turns and the resulting uncertainty. As UBS argues, the industry is “battle-tested”. It demonstrates a “capacity for self-correction, innovation and adaptation that has contributed to its continued expansion despite adverse conditions. This is relevant to every company: renewables reduce exposure to fossil supply risks while offering a more cost-efficient energy supply over time. This in turn creates financial room to diversify and invest in a “resilience premium” in other company segments.

Resilience, in other words, is no longer the art of bouncing back. It is the discipline of staying strategically capable.

4. Principles for Action in an Age of Geopolitical Disorder

If resilience is to become actionable, organizations need to move beyond the assumptions of the efficiency-first era without abandoning the gains that efficiency has created. The challenge is not to replace openness with closure or optimization with redundancy everywhere. It is to become more selective, more deliberate and more adaptive in how exposure is managed.

A first principle is selective openness. In a world of geoeconomic pressure, organizations cannot maximize exposure everywhere and then hope diversification alone will protect them. They need to distinguish between productive interdependence and dangerous dependence. Some connections create growth. Others create coercible vulnerability. Strategic resilience requires the ability to tell the difference.

A second principle is intelligent redundancy. The goal is not to duplicate everything. That would be inefficient and often impossible. The goal is to create redundancy where failure would be strategically costly: in critical suppliers, digital infrastructure, energy systems, data architecture, logistics routes, skills and governance. The question is never whether redundancy is expensive. The question is whether single-point fragility is more expensive.

A third principle is dynamic adaptation rather than static optimization. Traditional efficiency logic assumes a relatively stable external environment. That assumption no longer holds. Organizations need to optimize not only for cost, but for adaptability. That includes shorter decision loops, trigger-based playbooks, modular investments, reversible commitments and more deliberate scenario-based capital allocation.

A fourth principle is the integration of climate and AI into core strategy. Climate and biodiversity action cannot sit only in ESG or sustainability. It belongs in footprint strategy, capex planning, insurance, procurement, asset renewal and product design. AI cannot sit only in IT or innovation. It belongs in competitive positioning, technology architecture, cyber resilience, workforce strategy and governance. Both are strategic variables, not side topics.

A fifth principle is legitimacy. In an age of polarization and distrust, reputation and license to operate become harder assets. Organizations need credible positions on resilience, responsibility and public value. Not because narratives replace strategy, but because strategy without legitimacy becomes harder to execute under stress.

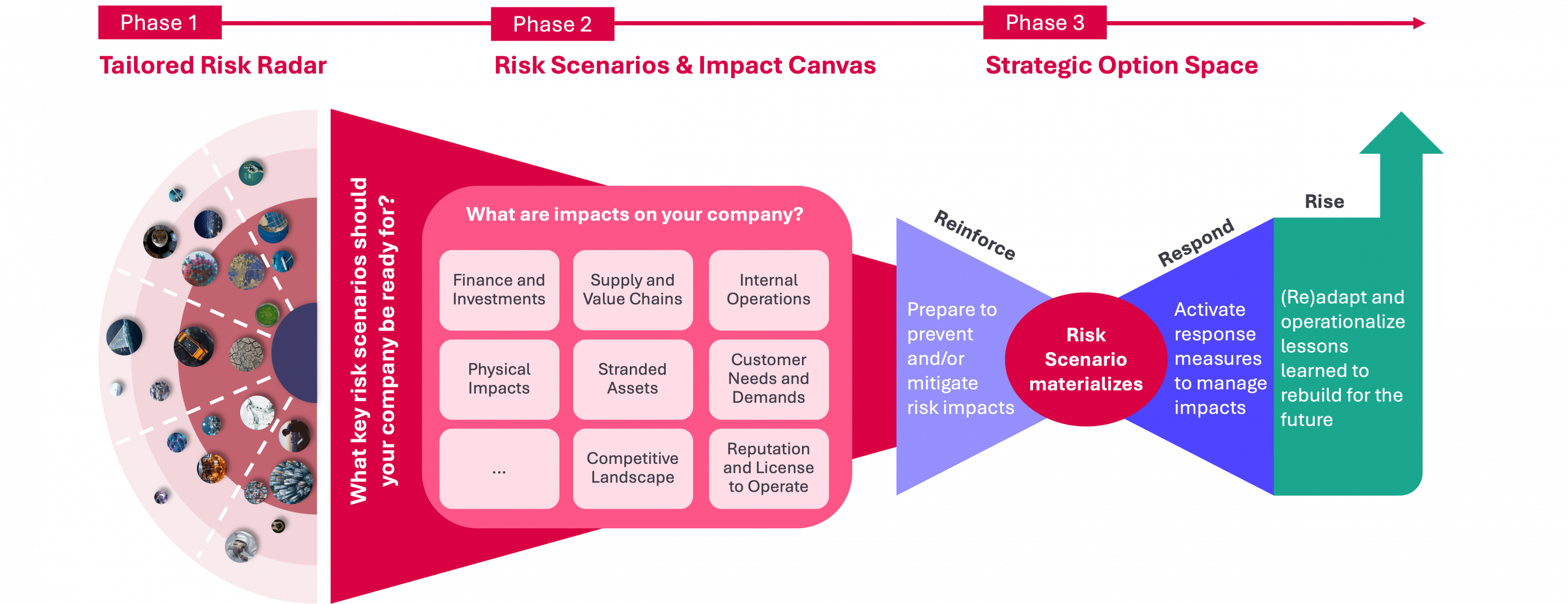

5. A Foresight-Based Process for Building Strategic Resilience

Because the challenge is systemic, the response cannot be limited to conventional risk registers or annual planning cycles. What is needed is a foresight approach that not only explores long-range uncertainty but systematically translates it into near-term strategic orientation and decision-making. In that sense, foresight must evolve into strategic resight: the ability to improve decisions today under conditions of persistent uncertainty.

This can be achieved through a prototypical three-step process that can be tailored to specific organizational needs and range from comprehensive analytical to focused interactive formats.

The first phase is a tailor-made 360° risk radar. The purpose is to build a shared outside-in and inside-out picture of the emerging risk landscape. Outside-in means scanning the external environment across society, technology, economics, ecology, and politics. As a starting point we draw on our set of Z_punkt Global Risks that we derived through our foresight-experience and research. The Z_punkt Global Risks put the age of geopolitical disorder into a broader risk context, for instance by considering nightmare competitors, shifting consumer needs and the potential slowdown in demographics and economic growth. Inside-out means examining the organization’s portfolio, footprint, dependencies, strategic ambitions and structural blind spots. The result is not a generic catalogue of risks, but a prioritized risk landscape specific to the organization’s exposure profile and strategic time horizons.

The second phase is a deep dive into risk scenarios and impact pathways. Prioritized risks are translated into plausible scenarios that show how they could build up, materialize and unfold over time. This matters because risk scenarios are rarely one-off events and emerge through the interplay of multiple risks. They have upstream drivers, trigger points and downstream impact cascades. A scenario-based impact canvas helps organizations identify where exposure is greatest across business fields, operations, resources, finance, customers, suppliers, partnerships, reputation and license to operate. In our projects we define indicators and signals for scenarios that should be monitored continuously.

>At this point, the value of foresight depends on whether it can inform decisions in the present.The objective is not only to understand how uncertainty may unfold over time, but to link long-term uncertainty with short-term strategic orientation. This means translating scenarios, signals and impact pathways into decision-relevant insights today: what requires attention now, which assumptions need to be challenged, and where early adjustments can improve strategic positioning before disruption fully materializes.

The third phase is the strategic option space. This is where foresight turns into action. Options are defined along the full risk timeline that follow the established bowtie model: reinforce before disruption, respond during impact, and rise beyond it. Reinforce means strengthening capabilities, governance, partnerships and buffers before a shock materializes. Respond means activating measures that protect operations, customers, people and value creation when disruption hits. Rise means adapting portfolio, footprint, investments and capabilities in ways that improve long-term position after the shock. This phase turns foresight into concrete decisions, owners, capability requirements and implementation priorities, distinguishing between no-regret moves, contingent bets and issues that require continued observation rather than immediate commitment.

The value of this approach lies in its practical orientation. It does not ask leaders to choose one forecast. It equips them to make better choices now across several plausible risk futures. It also creates the cross-functional dialogue that strategic resilience requires, because geopolitical, climate and technology risks do not respect organizational boundaries. That is especially valuable when leadership needs to optimize the next one to three years without weakening the organization’s long-term position.

6. What Organizations Should Do in the Upcoming Years

The immediate task is not to build perfect certainty. It is to raise preparedness, improve decision quality and protect optionality. Several no-regret moves stand out.

First, organizations should map dependencies that can be weaponized. This includes suppliers, logistics routes, raw materials, cloud providers, AI infrastructure, cybersecurity dependencies, energy exposure, regulatory dependencies and key regional revenue pools. The objective is not merely visibility, but prioritization: which dependencies are acceptable, which require alternatives, and which demand active de-risking.

Second, they should stress-test their portfolio and footprint against several external risk scenarios. These scenarios may differ in the intensity of trade fragmentation, the severity of climate impacts, the speed of AI concentration, the volatility of U.S. policy, or the degree of conflict escalation, for instance in regarding trade routes in the South China Sea. The aim is to understand where current growth assumptions are too fragile, where footprint decisions are too irreversible, and where strategic commitments require adjustment.

Third, organizations should create a clear AI resilience agenda. That means deciding where AI is mission-critical, where external dependence is acceptable, which use cases require tighter governance, how model and cloud concentration affect strategic autonomy, and how cyber resilience changes in a future with humanoid robots and ubiquitous AI agents. The winners will not be those who adopt AI fastest in a narrow sense, but those who adopt it with strategic discipline.

Fourth, climate and biodiversity risks should be embedded in the investment logic of the organization. Physical climate risk, water stress, heat and resource competition need to inform asset decisions, facility planning, supplier selection and business continuity assumptions. Organizations that treat adaptation as an afterthought will eventually pay for it in higher costs, lower reliability and reduced insurability.

Fifth, organizations should establish signposts and trigger points that connect monitoring to decisions. Too many early-warning systems stop at observation. Strategic resilience requires a different question: what development will trigger which decision? This converts risk scanning from an information exercise into a strategic management tool.

Sixth, they should build a bridge between crisis management and strategy. Most organizations have some form of response capability. Far fewer have a disciplined mechanism for learning from shocks and using them to reshape portfolio, partnerships, capex priorities and governance. Strategic resilience depends on that bridge.

7. How Z_punkt Can Support

<Z_punkt can support organizations by turning a diffuse sense of uncertainty into a structured strategic process. The starting point is not alarmism, but a rigorous view of how external change intersects with company-specific exposure. The task is to make uncertainty understandable, relevant and actionable.

What distinguishes a foresight-based approach is its combination of breadth and decision relevance. It captures geopolitical, geoeconomic, technological, ecological and societal developments in one integrated view, while translating them into concrete implications for business fields, functions, investments and leadership choices. This helps organizations move beyond silos and fragmented risk conversations as to develop a coherent resilience agenda.

In practical terms, this means helping leadership teams identify which external risks matter most, where blind spots are greatest, how risks could cascade across the organization, and which strategic options should be prioritized now. It also means sharpening short-term strategic orientation: where to reinforce, where to de-risk, where to partner, where to invest, where to build optionality, and where to accept exposure because it remains strategically worthwhile.

This is especially valuable in a short-term horizon of 12 to 36 months. In that window, organizations must often make decisions on footprint, sourcing, partnerships, digital architecture, AI use, capital allocation and strategic priorities before the world becomes more stable. Waiting for clarity is rarely a neutral option. It is often a decision in favor of passivity. Foresight, when applied rigorously, becomes strategic resight: it replaces passive observation with disciplined, decision-oriented preparedness.

Conclusion

The question for organizations is no longer whether geopolitics, geoeconomics, climate change and AI belong in strategy. They already do. The real question is whether organizations will continue to treat these forces as external turbulence, or whether they will turn them into a disciplined guard rail for strategic choice.

Strategic resilience is the capability to do exactly that. It enables organizations to preserve room for maneuver, act earlier, absorb shocks more effectively and emerge stronger from disruption. In a world defined by fragmentation, coercion, climate stress and technological acceleration, this capability will increasingly separate those who merely endure uncertainty from those who can use it to build future strength. And Foresight is a necessary lever to achieve strategic resilience.